The 3.6 billion dollar question

Documents seen by Josimar suggest that 777 Partners owed a total of 3.6 billion US dollars to creditors in the summer of 2023. Overdue debt-related payments totalling over 145 million dollars raises fresh concerns about the finances of the US group and its portfolio of clubs.

By Philippe Auclair and Paul Brown

A corporation the scale of 777 Partners borrowing millions by the tens, or even hundreds, in extraordinary circumstances is not rare. But there’s something peculiar about the amount of money they borrowed right before they reached an agreement to buy Everton. Josimar was able to view documents that showed 777’s corporate debt was far more than previously believed, totaling 3.6 billion US dollars in the summer of 2023.

According to Josimar, over the past few years, the Miami-based company has come to depend more and more on investor Kenneth King’s generosity to fund its operations. It’s estimated that King has given 777 at least $1 billion in of benefits through the businesses he owns under the A-CAP umbrella.

This number is the biggest outstanding principal on the website by a significant margin.As a “global business-to-business specialty finance company,” Credigy claims to be involved in the investment of “consumer-related assets.” In actuality, it mostly buys distressed debt in the US. Sixth-biggest bank in the nation, National Bank of Canada, acquired a majority share in Credigy in 2006 and went on to acquire 80 and then 100 percent of the company by the end of 2020. Credigy’s president and CEO, Louis Vachon, was quoted as expressing his pride in the company’s performance and how it “greatly exceeded our growth and return expectations.”Josimar has been informed that this 1.22 billion amount was borrowed against a sizable collection of structured settlements that 777 has bundled together. Credigy did not respond to Josimar’s request for clarification. But in a set of financials for 2021, also seen by Josimar, this debt to Credigy actually stood even higher at 1.418 billion, with the collateral for the loan described as “structured settlements and lottery receivables.” Much of 777’s early money was made in structured settlements – which are annuities commonly paid to settle personal injury claims. But they have proved to be a source of controversy for the firm, as Josimar has shown.

“Critical” situation

By August of 2023, this debt to Credigy accounts for a third of the 3.6 billion total borrowings by 777 at this point in time, a total which would not necessarily be of concern in itself if the group’s finances were healthy enough to sustain that level of debt and service it accordingly. This does not appear to be the case. According to the data Josimar has seen, as of last summer, 777’s overdue debt servicing payments to their corporate creditors totalled 147.2 million US dollars, of which 52 million were owed to A-CAP alone (*).

Not on the list were the creditors of their football clubs, who also suffered greatly. Another set of data revealed that Standard de Liège’s suppliers were overdue by a total of 4.4 million dollars for at least 240 days, or eight months, past the scheduled date of payment. Meanwhile, a $4 million loan from Bruno Venanzi, the club’s former owner, remained unpaid and accrued interest to the point where one of the documents referred to the situation as “critical” (*). Josimar is aware that the loan is still unpaid after six months.These are concerning figures given that Belgian media reports indicate that Standard’s eligibility to compete in the Belgian elite in 2024–2025 is far from guaranteed by the league’s regulatory body. Especially since we understand that 777 Partners and its sister company 600 Partners still haven’t produced audited accounts for 2020, 2021, or 2022. Standard de Liège’s Chief Executive Pierre Locht did not respond to Josimar’s inquiries.

The additional data that we examined further demonstrated that clubs under 777 ownership were having a very hard time paying their employees on time. This was evident at Vasco da Gama, Standard, and Genoa, where a million dollars that was supposed to have been paid in early June 2023 was still outstanding more than two months later. The losses those three clubs were predicted to suffer in the upcoming months were far worse. When autumn 2023 rolled around, Standard, Genoa (who didn’t answer Josimar’s questions either), and Vasco da Gama were estimated to be 24, 28, and 34 million dollars in the red, respectively, with no sign of a quick turnaround in their balances. London Lions, the basketball team of 777, was not anticipated to perform better, with a negative balance of just under 10 million dollars by All Saints Day.

Where can the money come from?

It may have been possible for 777 Partners to redress the balance in the months which have elapsed since, but fresh sources of financing seem to be getting harder and harder for them to find. The downgrading by credit agency AM Best of their Bermuda-based reinsurance arm 777re from “fair” to “weak” last month was a blow in itself. 777re had been a steady provider of funds for the operation of some of their more problematic assets, including budget airline Flair – which, contrary to leaks echoed in some media, failed in its attempt to merge with another budget airline, Lynx, in February (*) – and their portfolio of football clubs. But that was not all. Under pressure from the downgrading, one of 777re’s main backers announced that it would “exit from the relationship entirely” and that “within 45 to 60 days recapture all of the business”. That backer is none other than Kenneth King himself, who announced his decision during a webinar which Josimar attended. If, as he claimed, AM Best’s downgrading of 777re was “just a little bit of noise in the reinsurance sector”, it was a “little bit of noise” which was loud enough to be heard everywhere in the football world, including at Goodison Park.

This is due to the fact that, as Josimar stated, King and A-CAP are financing 777’s acquisition of Everton through working capital loans that A-CAP businesses have provided to the team. During a quick Q&A session following King’s webinar, one participant made an attempt to bring up this matter by enquiring, “Does A-CAP have exposure to the planned acquisition of Everton Football Club?” King ended the conversation early rather than responding to the question or a few others.

The issue for King with the recapture of his companies’ assets from 777re though, is that it requires the approval of the Bermuda Monetary Authority and the Utah Insurance Commission. Josimar has revealed both of those regulatory bodies have launched probes in which questions have been asked of A-CAP’s relationship with the reinsurer. It is not a given that approval will be granted.

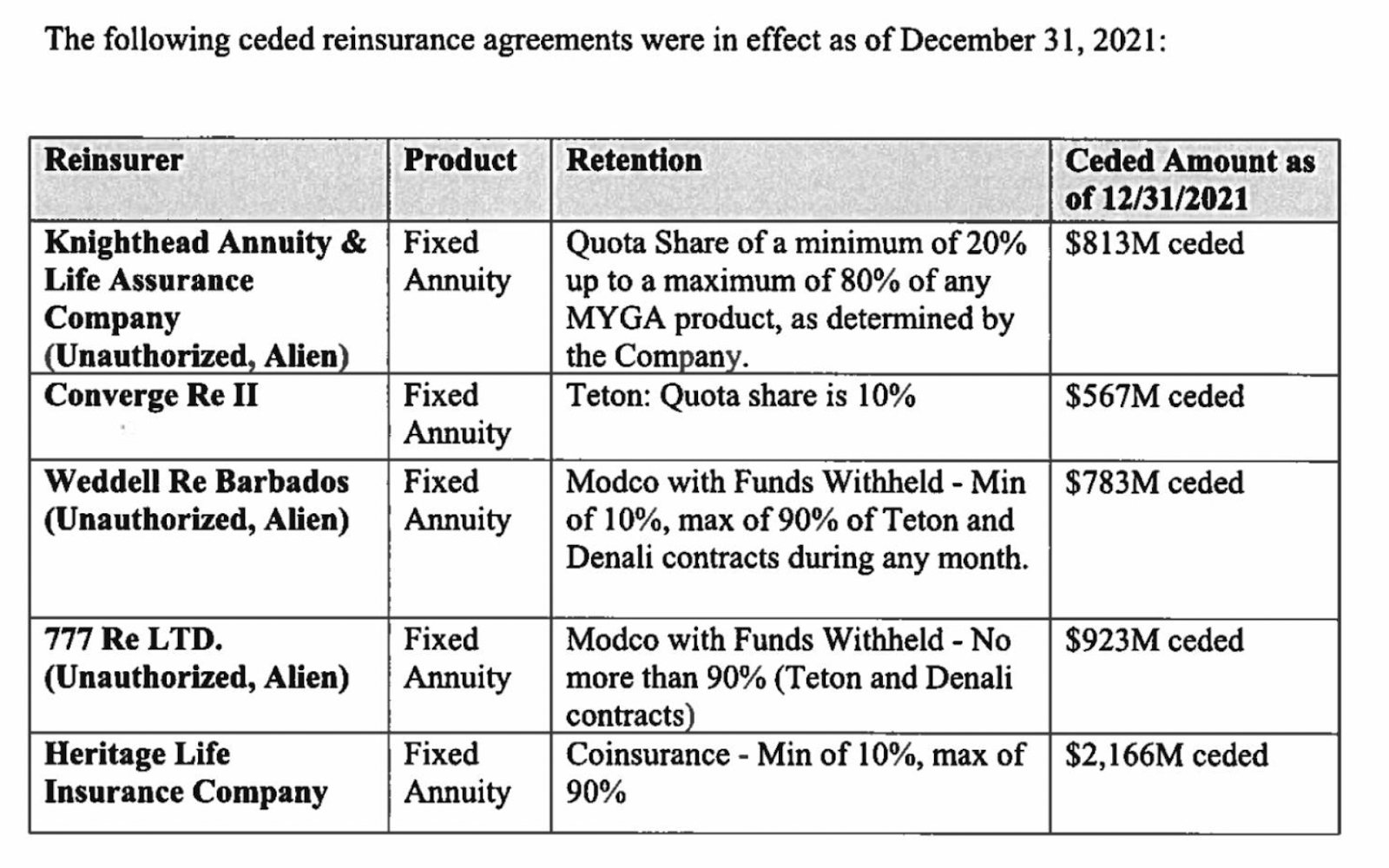

However, King is not the only lender or business associate attempting to cut ties with 777re and its affiliations with subsidiaries of 777 Partners at this time. According to multiple individuals that Josimar has spoken with, Utah-based SILAC Insurance Company is doing the same (*). Flair, a budget airline operated by 777, was given a sizable loan by SILAC, which has subsequently been written off. As of December 31, 2021, SILAC had 923 million dollars in assets “ceded,” or invested, in 777re. This could be due in part to SILAC’s downgrade from “stable” to “negative” by AM Best in December of last year, and their subsequent placement “under review with negative implications” in early February of 2024 due to their “heavy dependence on reinsurance” business, which includes 777re.

SILAC began life in 2020 as the new name for Equitable Life & Casualty Insurance Company, which was licensed in 47 US states and focused on life and health insurance for senior citizens before moving into the annuity market. Hildene Capital Management, a credit-focused asset manager, has since taken a stake in SILAC as part of a “long-term strategic alliance” between the firms.

SILAC’s chairman and CEO is Indiana businessman Stephen Hilbert, a one-time business partner of Donald Trump who once sold the former US president a Caribbean mansion, and who founded US insurance and finance company Conseco Inc, which went bankrupt in 2002.

With two of its major partners unwinding their relationship with 777re, a business which was described as the “anchor” of 777’s sales pitch to investors in 2021, it is easy to see why concerns have been raised.

Other data seen by Josimar indicates that 777 intended to address their August shortfall by securing a total of 1.2 billion dollars in fresh investments, namely by raising capital with the assistance of Tifosy Capital (Wander had mentioned “a few hundred million” in an interview with the Financial Times), securing new loans and refinancing deals including a proposed agreement with CitiBank worth several hundred million, and selling two of their assets, Merit Life Insurance and Sutton National, for a combined 345 million. None of these plans appear to have come to fruition yet. Some business media reported that Merit Life, owned by 777 affiliate Brickell Insurance Holdings LLC since 2020, had entered into a “definitive agreement” with an unnamed private investor back in September 2023, but no official announcement has yet been made, more than five months later. As to Sutton National, information received by Josimar suggests that the prospective buyer, believed to have been Boston-based company Charlesbank Partners, has now walked away from the agreement.

A representative for 777 informed Josimar that purchasers had been found for Merit Life and Sutton National when he was questioned about these planned operations. However, the representative withheld the specifics of the agreements, citing confidentiality. Additionally, the representative informed us that 777 Partners had not requested funds or an infusion of capital from CitiBank and that the Tifosy Capital raise had been suspended, with plans to resume if and when the Premier League approves the purchase of Everton FC.

When Josimar questioned 777 about alleged conversations with US businessman and Birmingham City FC owner Tom Wagner—with whom Wander was spotted in talks in London at the Financial Times’ Business of Football Summit 2024—777 declined to comment further. In addition to being a co-founder of Knighthead Capital Management, Wagner is also co-Chaiman of the Cayman Islands-registered Knighthead Annuity & Life Assurance Company, which also has ties to SILAC.

In any case, little if any of the 1.2 billion it was hoped would bring some oxygen into 777 Partners’ operations appears to have been pumped in as of yet.

Why Everton?

The same question keeps coming up: how is it that 777 Partners was able to agree to buy Everton just a few weeks later, in September, and that they have since been able to make loans to the club totaling almost 200 million GBP, when, as of last August, their debt situation was of such concern and the prospects of raising new finance so urgent? In addition, given Everton’s own financial difficulties, there is no assurance that they would receive all of the money they had to borrow back. Should their wait for the Premier League to approve that takeover prove futile, they are not even the first creditor in line. This represents a very risky enterprise which can be read two ways – either as a demonstration of confidence, courage and determination, or the last throw of the dice of a gambler who’s lost at almost every table he’s sat at before.

(*) When Josimar contacted 777, the company declined to comment on those figures; however, a representative for the group informed us that the numbers were incorrect, without disclosing the actual values.

(*) Red Star FC’s suppliers were also in arrears, but for a relatively little sum (24,000 US dollars), and at that point, they had only put in an additional three months of waiting.The London Lions basketball team performed the lowest in comparison, despite having a low turnover rate. It owed 1.4 million in delinquent taxes in addition to 385,000 dollars in outstanding contractor costs.

(*) Since then, Lynx has stopped operating and has received an initial injunction from the Court of King’s Bench of Alberta providing creditor protection.

(*) Reinsurance industry specialist Matt Zagula claims that SILAC’s exposure to 777re now amounts to 1.42 billion US dollars.

Read more news on:sportupdates.co.uk

Leave a Reply